There’s a version of your exit that goes well. Clean financials, multiple interested buyers, competitive offers, a smooth diligence process, and a final sale price that reflects the actual value of what you built. You transition out on your terms. The team stays intact. The business keeps running.

Then there’s the version most SMB owners actually experience. Rushed preparation, messy books, buyers who poke holes in everything, retrades that shave 15 to 20% off the agreed price, and a closing process that feels more like a hostage negotiation than a business transaction. Or worse, no deal at all because the business simply wasn’t ready.

The difference between these two outcomes is not luck. It’s not market timing. It’s not finding the right broker. It’s the five years of financial work that happens before you ever list the business. And for most owners, that work either starts too late or never starts at all.

This is the roadmap. Year by year. What to do, when to do it, and why each step matters. Whether you plan to sell in five years, three years, or just want to build a business that’s worth something beyond your personal involvement, this is the sequence.

Why Five Years (And Why Starting Now Isn’t Optional)

Five years sounds like a lot of runway. It’s not. Every phase in this roadmap builds on the one before it, and skipping steps or compressing the timeline means you show up to the deal table with gaps that buyers will find and price into their offer.

According to the Exit Planning Institute, an estimated 73% of privately held companies in the U.S. plan to transition ownership within the next decade, representing a $14 trillion opportunity. But planning to transition and being prepared to transition are two very different things. A U.S. Bank survey found that while 85% of business owners started their company to create something they could pass on, only 54% have a formal succession plan in place. And 62% say the process of navigating succession feels overwhelming.

The owners who exit well are the ones who gave themselves enough time. Time to clean up the books. Time to build a financial team. Time to identify and pull the levers that actually grow EBITDA. Time to prepare for the scrutiny of due diligence. And time to go to market with a business that buyers compete for, not one they discount.

McKinsey estimates that by 2035, six million SMBs will need new ownership as founders retire. In 2022 alone, 92% of business exits ended in closure, not a sale. Not because the businesses lacked value, but because the infrastructure for succession was never built.

Source:

McKinsey Institute for Economic Mobility, “The Great Ownership Transfer” (2025)

Here’s what each year looks like.

Year 5: Get Your Books Right

Everything starts here. If your financial foundation is broken, nothing you build on top of it will hold up. This is the year you stop treating your books as a tax compliance exercise and start treating them as the financial operating system of a business that will eventually need to withstand buyer scrutiny.

Most SMB owners don’t realize how far off their books actually are until someone with transaction experience looks at them. The chart of accounts isn’t structured to show revenue by type or expenses by department. Revenue and cost of goods sold are lumped together in ways that make margin analysis impossible. Personal expenses are mixed into operating costs. Monthly close doesn’t exist. The CPA sees the books once a year, rebuilds what they can, and files the return.

This is the starting point for the majority of businesses in the $1M to $20M range. And it’s not a moral failing. It’s just what happens when the financial infrastructure was built for tax compliance and survival, not for strategic decision-making or eventual sale.

What Needs To Happen In Year 5

The chart of accounts needs to be rebuilt or restructured to reflect how the business actually makes money. Revenue should be segmented by type: recurring versus one-time, by service line, by product category. Cost of goods sold needs proper mapping. Operating expenses need departmental classification. If you have multiple entities, they need to be consolidated properly.

A monthly close process needs to be established with a defined timeline and clear ownership. The target should be a closed set of books by the 15th of the following month, no later than the 21st. If your books currently close once a year at tax time, this is the single biggest shift you’ll make.

Bank and credit card reconciliations need to be current. Revenue recognition needs to be consistent. AP and AR need structured workflows. Payroll needs to be clean and properly documented.

This sounds basic. It is basic. But the number of businesses doing $5M, $10M, or $15M in revenue that don’t have these fundamentals in place is staggering. And every single issue on this list becomes a problem during diligence if it’s not fixed years in advance.

A medical device distributor managing $15 to $20M in gross sales flow came to the table with no QuickBooks file, no chart of accounts, no monthly close, and a founder personally handling payroll and commission tracking across email threads. The CPA only saw the books once a year. Getting that cleaned up and structured wasn’t a one-month project. It required implementing an accounting system from scratch, designing the chart of accounts around the business model, establishing a monthly close process, and building the documentation infrastructure that made the numbers trustworthy for the first time. That kind of work takes time, which is exactly why it starts in Year 5.

Year 4: Build Your Financial Team

Your books are clean. You have a monthly close. Now you need the people and the systems to turn those numbers into something that actually drives decisions.

This is the year you bring in financial leadership. For most SMBs in the $1M to $44M range, that doesn’t mean hiring a full-time CFO at $250K or more per year. It means engaging a fractional CFO who has transaction experience and can start building the financial infrastructure that will eventually need to hold up under buyer scrutiny.

What A Fractional CFO Does In Year 4

The first priority is getting real visibility into the business. That means building financial dashboards with KPIs that are tied to actual performance: gross margin by product or service line, customer-level profitability, cash reserve coverage, operating efficiency metrics, and DSO trends.

The second priority is establishing a forecasting and budgeting discipline. A rolling 12-month forecast tied to growth targets. Budget models connected to operational strategy. Scenario planning that lets you model what happens if revenue drops 10% or if a key client leaves.

The third priority is cash flow management. A 13-week rolling cash forecast that maps inflows against committed outflows. If you have working capital volatility (seasonal businesses, inventory-heavy businesses, businesses with long collection cycles), this is where you get it under control.

This is also the year you start aligning your advisory team. Your CPA handles taxes. Your fractional CFO handles strategic finance. Your bookkeeper or controller handles the day-to-day. These three roles need to be talking to each other, and in most businesses, they aren’t. Getting them coordinated early avoids the last-minute scramble that happens when a deal is on the table and nobody’s aligned.

A boutique consulting firm with a full pipeline and recurring cash flow gaps brought in Frak Finance to build a KPI system and financial dashboard. Client profitability had never been tracked at the engagement level. Pricing was set without contribution margin analysis. Within one engagement cycle, client profitability increased 18%, cash flow gaps were cut in half, and leadership shifted from making decisions on gut feel to making them off real data. That’s what Year 4 looks like when it’s done right.

Year 3: Identify Your EBITDA Levers

You’ve got clean books and financial visibility. Now it’s time to make the business more valuable. EBITDA is the number that drives valuation in most SMB transactions, and this is the year you get intentional about growing it.

EBITDA growth doesn’t just mean more revenue. In fact, revenue growth without margin improvement can actually make things worse if it comes with compressed margins or increased working capital strain. The smarter approach is to find the levers that improve profitability without requiring proportional increases in cost or complexity.

Where EBITDA Improvement Actually Comes From

Vendor renegotiations are one of the most reliable levers. Most businesses haven’t reviewed their vendor contracts in years. Renegotiating terms on your top five or ten vendors, whether that’s raw materials, software, shipping, or professional services, can meaningfully improve gross margin without changing a single thing about how you sell.

Pricing adjustments on undervalued products or services are another major lever. This requires the margin-by-line visibility you built in Year 4. Once you can see which products or service lines are actually profitable and which ones are consuming more resources than they return, you can adjust pricing or de-emphasize low-margin work.

Operational cost reduction is the third lever. Not arbitrary cost-cutting, but targeted elimination of inefficiencies: redundant tools, underperforming roles, processes that consume time without producing proportional value. The goal isn’t to run lean to the point of fragility. It’s to remove the waste that’s compressing margins without adding value.

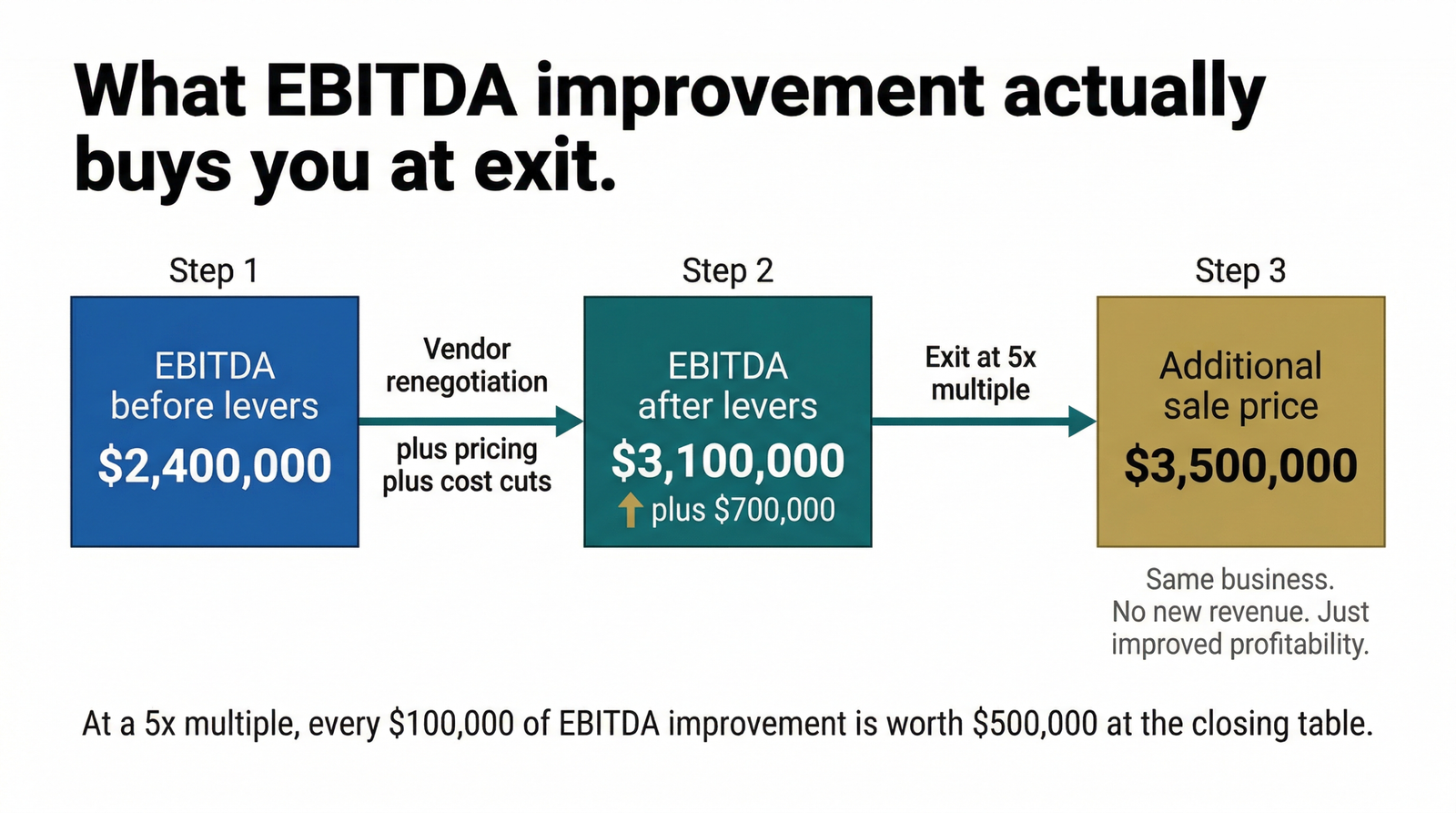

A family-owned manufacturer with $18M in revenue and $2.4M in EBITDA used exactly this playbook. Vendor renegotiations improved gross margin. Operational waste was cut. Underpriced SKUs were repriced. The sales focus shifted toward higher-margin and recurring revenue. EBITDA grew 30% over 24 to 30 months, from $2.4M to $3.1M. At the eventual 5x exit multiple, that $700K in EBITDA improvement was worth $3.5M in additional sale price. That’s not revenue growth. That’s financial engineering on the existing business.

Revenue Diversification Starts Here Too

Year 3 is also when you start addressing customer concentration. If any single client represents more than 25 to 30% of your revenue, that’s a valuation discount waiting to happen. Buyers price concentration as risk, and they’re right to do so.

The fix isn’t overnight. It requires targeting new mid-tier accounts, expanding into additional channels, strengthening contract terms with existing clients, and building pipeline tracking so you can measure the mix shifting month over month. This work takes 12 to 18 months to show results, which is why it starts in Year 3 and not Year 1.

According to Gallup, 27% of employer firms with owners aged 55 and older are either unsure of their long-term plan or intend to close the business permanently. Employer firms that plan to sell report median profits of $100,000, compared to just $20,000 for those that plan to shut down. Planning pays.

Source: Gallup,

“Most Small-Business Owners Lack a Succession Plan” (2025)

Year 2: Prep for Due Diligence

Your financials are clean. You have financial leadership. EBITDA is trending up. Customer concentration is coming down. Now it’s time to pressure-test everything from the buyer’s perspective.

Due diligence is not a financial review. It’s a stress test. The buyer’s team is looking for every reason to lower their offer, renegotiate terms, or walk away. Your job in Year 2 is to make sure there are no surprises.

EBITDA Normalization And Documentation

Every owner add-back, every discretionary expense, every one-time cost that inflates or deflates EBITDA needs to be identified, documented, and tied to source material. This is the foundation of the Quality of Earnings process, and if you wait until you’re under LOI to start doing this work, you’re already behind.

Common add-backs include above-market owner compensation, personal expenses run through the business, one-time legal or consulting fees, non-recurring contractor costs, and family members on payroll who don’t work in the business. Each one needs a paper trail. An adjustment without documentation is an adjustment that a buyer will challenge.

Operational Transferability

This is the year you prove the business can run without you. That means documented SOPs across the functions that matter: procurement, fulfillment, sales, customer management, financial reporting. It means elevating key managers into leadership roles where they’re making decisions, managing relationships, and executing strategy without the founder in the room.

An $8M e-commerce company preparing for sale spent this phase documenting SOPs across procurement, fulfillment, and sales management. They moved key customer relationships off the founder and onto the broader team. They built a management structure outline that showed buyers the business runs without the owner. By the time buyers started looking, nobody was asking about risk. They were asking about growth.

Working Capital And Cash Flow Stability

Buyers look closely at working capital patterns to determine how much cash the business needs to operate on a day-to-day basis. Volatile or poorly managed working capital gives buyers leverage to negotiate a higher working capital peg at close, which directly reduces the seller’s cash proceeds.

Year 2 is where you stabilize these patterns. Get receivables collected faster. Negotiate better vendor terms. Clean up inventory if applicable. Build a working capital analysis that tells a clear, consistent story.

Year 1: Go to Market with Confidence

Everything you’ve built over the last four years comes together here. The books are clean and buyer-ready. The financial team is in place. EBITDA has been growing for 24 to 36 months. Customer concentration is manageable. The business runs without the founder. Working capital is stable. Documentation is airtight.

Pre-Market Positioning

Before you engage a broker or start conversations with potential buyers, you should have a complete financial package ready: normalized EBITDA with a documented adjustment schedule, three to five years of consistent financial statements, margin analysis by product or service line, a working capital analysis, and a forward-looking forecast that shows the business has a plan.

This is also when you finalize your buyer profile. Are you targeting a strategic acquirer who will integrate your business into their platform? A private equity firm that will install professional management and grow? A competitor looking for market share? A management buyout where your team takes over? Each buyer type values different things, and the way you present the business should reflect that.

The QOE: Do It Before They Do

Consider commissioning a seller-side Quality of Earnings report. This lets you find and fix any remaining issues before a buyer’s diligence team finds them for you. The cost of a seller-side QoE is a fraction of what a retrade costs. And the signal it sends to buyers, that you’re serious, prepared, and transparent, changes the tone of the entire negotiation.

A SaaS company with $750K in ARR almost lost a $4.5M deal because their buyer-initiated QoE failed. Revenue was mixed. Adjustments were undocumented. The deal stalled. They got lucky because the financials were rebuilt in time. Most sellers don’t get that second chance.

Multiple LOIs And Negotiation Leverage

If you’ve followed this roadmap, you should be in a position to attract multiple interested parties. That’s not a nice-to-have. It’s the single biggest driver of negotiation leverage in a transaction. Multiple LOIs mean you’re not negotiating from necessity. You’re choosing the best offer from a position of strength.

The manufacturer that followed a three-year version of this roadmap received multiple indications of interest above their initial informal valuations. The e-commerce company that prepped for 18 months had multiple buyers competing. In both cases, the competition among buyers is what pushed the final price above expectations. That competition doesn’t happen by accident. It happens because the preparation made the business attractive enough to create it.

What Happens If You Start Late

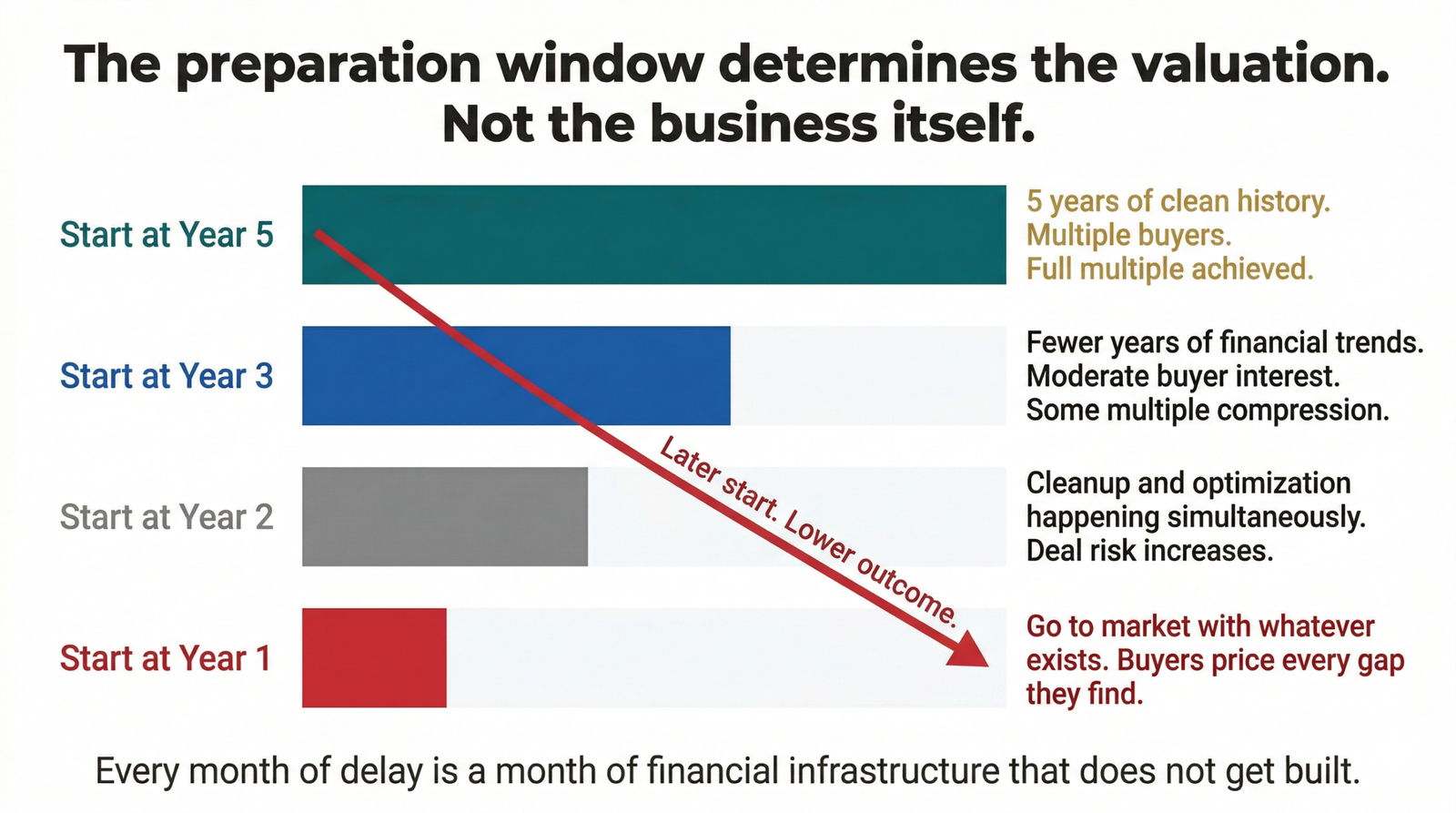

You can compress this timeline. People do it all the time. But compression has costs.

Starting at Year 3 instead of Year 5 means your books might be clean but you’ll have fewer years of consistent financial history to show. That limits what a buyer can trend. Starting at Year 2 means you’re doing financial cleanup and EBITDA optimization simultaneously, which creates strain on the business and risks the very revenue decline that tanks valuations during the sale process. Starting at Year 1 means you’re going to market with whatever you have, and whatever you have is what buyers will pay for.

The Pepperdine Private Capital Markets Project found that businesses experiencing revenue declines during the sale process saw valuations drop 15 to 20%. That decline usually happens because the owner is so consumed by the deal that they take their foot off the gas operationally. When you start early, you have the capacity to sell the business while still running it at full speed. When you start late, something has to give.

There are 2.9 million businesses in the U.S. owned by individuals aged 55 or older, supporting 32.1 million employees, $1.3 trillion in payroll, and $6.5 trillion in revenue. What happens to those businesses over the next decade depends entirely on whether their owners start planning now or wait until it’s too late.

Source:

Project Equity (2025)

Every month you wait is a month of financial infrastructure, EBITDA improvement, and operational restructuring that doesn’t happen. The math isn’t complicated. Start earlier, exit better.

The Bottom Line

This roadmap isn’t theoretical. Every step maps to real work that real businesses have done to exit at higher multiples with fewer complications. Clean books in Year 5. Financial leadership in Year 4. EBITDA optimization in Year 3. Diligence preparation in Year 2. Market entry in Year 1.

The businesses that follow this sequence don’t just sell. They sell well. Higher valuations, smoother diligence, multiple buyers at the table, and founders who walk away knowing they captured the full value of what they built.

The businesses that skip it leave money on the table. Sometimes a lot of it.

Whichever year you’re in right now, that’s where you start.

Where to Go From Here

If you’re three to five years out from a potential exit, or even if you’re just building a business you want to be worth something beyond your daily involvement, this roadmap is how you get there. But knowing the steps and executing them are two different things.

At Frak Finance, we work with SMBs across every phase of this timeline. From bookkeeping cleanup and chart of accounts restructuring, to fractional CFO leadership with KPI frameworks and forecasting, to EBITDA optimization, QoE preparation, and full M&A advisory. We’ve helped businesses go from unprepared to buyer-ready, and we’ve seen firsthand what the difference in preparation is worth at the closing table.

Schedule a free consultation and let’s figure out where you are on this roadmap and what the next twelve months need to look like.